People active in the securities industry likely have at least a general understanding of how the SEC recoups the funds that Congress appropriates to it under Section 31 of the Securities Exchange Act of 1934. And most are probably aware that fee rates charged under that provision have fluctuated widely from year to year, for many years. But participants likely do not appreciate the practical impact that these fluctuations may have on the trading market for certain securities, especially exchange-traded funds (ETFs), and how the fee-setting system affects them. This post has two main objectives:

- To summarize an analysis IEX has conducted that suggests there is a significant unintended and disruptive impact of changes in the Section 31 fee on the trading of certain securities, and ETFs in particular; and

- To suggest a targeted change to Section 31 that would allow the fee to be set and adjusted each year in a way that is more predictable and reduces these negative impacts.

Background

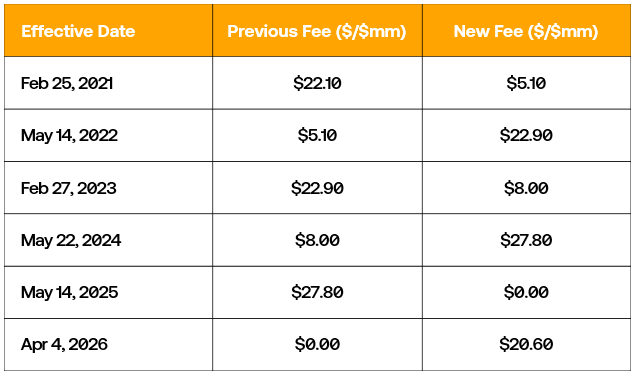

Like most other federal agencies, the SEC’s funding depends on an annual appropriations process. Unlike most other agencies, the law directs the SEC to “recover” the cost of each year’s appropriation, and Section 31 prescribes the process by which it does so. In general, the SEC is required to set a rate that is charged on the dollar amount of “covered sales” of exchange-traded equities and options (there are special provisions for how the rate applies to options). The statute contemplates that the SEC will set a baseline fee rate around the start of the government fiscal year, which begins October 1, and then reset the rate in the middle of the fiscal year – more on that later. Section 31 lays out the methodology to be used to project covered sales, and the SEC publishes its analysis whenever it resets the fee.

The fees are collected in the first instance by the securities exchanges and FINRA from their members (the Options Clearing Corporation facilitates the payment of fees on options transactions) and then passed on to the government. Those members that can do so typically pass those fees along to their customers in the form of a “Section 31 fee” typically designated as such on trade confirmations.

The Rollercoaster Effect and the Impact on Trading

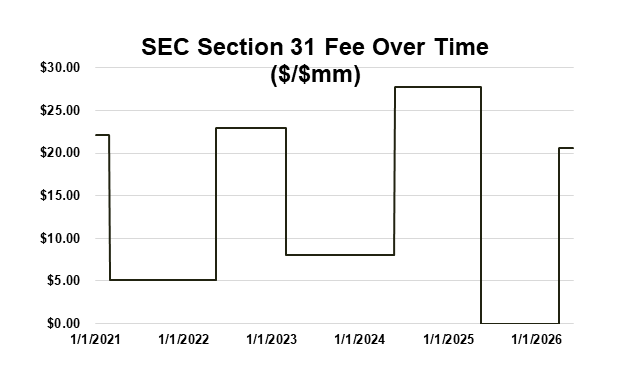

If Section 31 is meant to allow for regulatory fees that are relatively predictable and stable, the result has been very different. In fact, fee rates have tended to gyrate annually from high to low and back again as seen by the following charts:

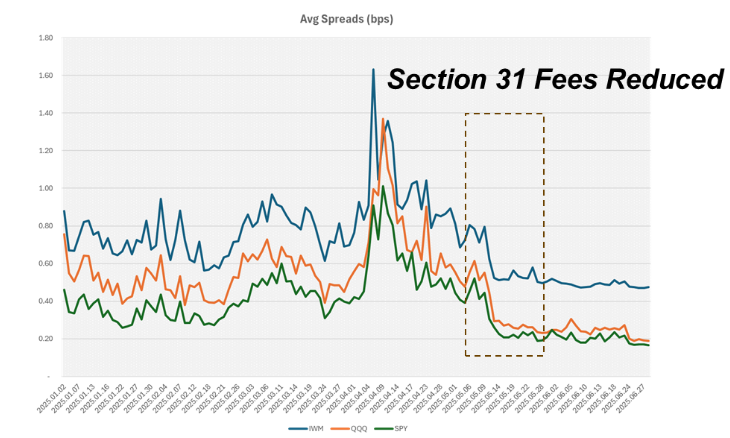

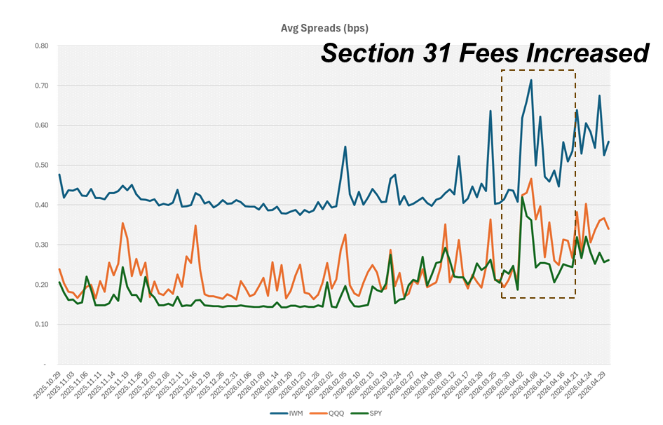

More important, data analyzed by IEX suggests that this variance has a real impact on trading behavior for ETFs in particular, as measured both by average spread and trading volumes. First, here is a look at the change in the average quoted spreads of some benchmark, high-volume ETFs – QQQ, SPY, and IWM (the Russell 2000 index ETF), comparing results when the rate fell to 0 from $27.80 per million in covered sales on May 14, 2025, and then rose from 0 to $20.60 on April 4 of this year.

The charts indicate there was a significant and persistent decrease in quoted spreads beginning on the first date the 0 fee was in effect and an even more dramatic increase in spreads beginning when the fee was reimposed at a high level in April of this year.

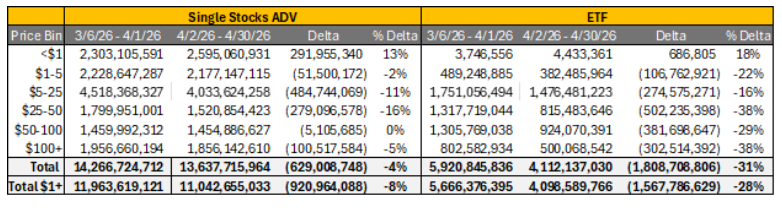

We also looked at overall trading volumes across ETFs. Here, we focused on the impact of the dramatic fee spike in April 2026, comparing the several weeks immediately before and after the change. To have a basis for comparison of ETF volume, we looked at volumes for both single stocks and for ETFs, and further divided the data by various price “buckets”.

This data shows that there was a significant decrease in volume for ETFs relative to single stocks in every price category,i and the amount of the difference tends to grow as the per share price increases. That result might be expected given that the rate is charged on dollar volume, rather than per share, and so abrupt changes in the fee stand to have a bigger impact on the trading costs of higher-priced ETFs.

We think the data on spreads and volume strongly suggests that fee rate changes can have a meaningful impact on trading behavior, particularly the trading of high-volume, high-priced, low-margin securities such as many ETFs, for which each aspect of all-in costs makes a difference to participants trading them. Although we do not have a clear view into the potential impact on options, it stands to reason Section 31 fee levels could have a meaningful impact on trading of at least some options contracts that have the same types of characteristics.

What Is the Source of the Problem?

The root of this problem is simple enough to understand. Section 31 as written ties the SEC’s ability to set and adjust the fee to the timing of its full year appropriation. Under the law’s design, the SEC is meant to establish a new rate around the start of the fiscal year (October 1) based on the assumption it has received a full-year appropriation by that time. The new rate is effective 60 days after the appropriation is passed. Section 31 also calls for a mid-year (April 1) adjustment to the rate based on experience and updated analysis from the first half of the fiscal year. To avoid the need to change systems to account for relatively minor fee differences, this mid-year reset occurs only when the SEC projects that a revised projection of the volume of covered sales for the year would vary by 10% or more from the baseline estimate.

In practice, the SEC, like many other agencies, typically does not receive a full-year appropriation before or near the start of the fiscal year. More often, it relies on funding in the form of a “continuing resolution” (CR) that keeps funding at current levels, until an appropriation bill is enacted later in the year. During periods covered by a CR, the SEC is required to keep in place the preexisting fee rate and can only set a new rate effective 60 days after the appropriation is enacted. In practice, this means that the fee is reset at unpredictable intervals well after the start of the year. It also means that the ability to adjust mid-year is mooted, which causes the rate to be based on outdated data for long stretches of time.

How to Improve the Process

For years, many in the industry have argued that Section 31 fees should be paid by participants beyond those in equities and options, to include other markets regulated by the agency – the fixed income markets in particular.ii Those are valid concerns, but proposals to increase the scope of payers are by nature highly controversial, and those questions are unlikely to be resolved any time soon.

As an intermediate step, we suggest a relatively simple and targeted change to Section 31 to even out the rollercoaster. First, if the SEC receives a full appropriation before the start of the fiscal year, the provision would operate as written, with a new rate set on or close to the beginning of the year and adjusted mid-year as needed. Otherwise, the provision would call on the SEC to set the rate as of October 1 based on the funding level then in effect, using the latest data to estimate future market volume. The rate would then be reset when the appropriation is received, taking into account the appropriated amount and refreshed data on market volumes. In setting or resetting the rate, the SEC would continue to use the methodology the statute prescribes, and its analysis would continue to be fully transparent.

This alternative would not work as well if the SEC received its appropriation relatively soon after the start of the fiscal year. In that case, the SEC could be called on to set different rates in quick succession. But that could be solved with the proviso that a new rate cannot be set until a minimum number of months have elapsed since the last reset. Further, the statute could retain the existing caveat eliminating the reset when it would have a minimal impact on the fee rate.

There are some variations on this general approach that could be viable. For example, the rate might be always set on October 1 and always reset on April 1, or at quarterly intervals (subject to the 10% threshold) regardless of the timing of the appropriation. That would maximize predictability but might be viewed as unduly separating the process for recovering appropriated funds from the appropriations. Regardless, it should be clear that any change to Section 31 would not and should not affect the appropriations process itself. Instead, the sole focus would be to make the process of recovering appropriated funds more rational and less prone to unintended side-effects.

Even small changes in law and regulation can have a meaningful impact, and when they are grounded in common sense and can garner consensus support, the chances for success become much greater.

i The market for sub-dollar stocks is heavily driven by ephemeral retail investor sentiment and other indigenous factors that we believe reduce the relevance of this category for purposes of this analysis.

ii Regarding the collection of fees from equities markets, as the Commission considers proposals to permit the “tokenization” of equities securities, it also seems logical that any trading of those equities should trigger payment of a Section 31 fee commensurate with that paid by persons trading non-tokenized equities. Otherwise, the ability to avoid the fee would reduce the cost of trading a token compared to the underlying stock, creating a form of government-sponsored regulatory arbitrage.

Chief Market Policy Officer

Head of Business Analytics