In early March, IEX Exchange launched an optional new functionality for our D-Limit order type, designed to improve hit rates without sacrificing performance. So far, so good! The results have been encouraging, and we’re excited to share preliminary data illustrating the improved experience early adopters have enjoyed.

As we wrote in previous blogs on the subject, D-Limit is designed to deliver genuine spread capture and avoid adverse selection. When you send a displayed D-Limit order to IEX Exchange and the Signal predicts that the price is likely to change, we reprice you one tick outside the unstable price, which is usually the NBBO. Say the NBBO is $5.10 x $5.11, and you send a displayed D-Limit to buy with a $5.10 limit and the Signal predicts that the $5.10 bid is about to crumble. D-Limit moves your $5.10 buy order one tick more passively to $5.09, and IEX Exchange sends you a FIX message back with $5.09 as the new effective limit on your order. This is what we call the “restatement message”.

That “restatement message” allows brokers to decide whether they are happy with their new resting price, or whether they wish to act upon their order to change it. However, firms who do not consume the restatement message are, at times, flying blind. If, in the above example, IEX Exchange moved the D-Limit order to $5.09, but the National Best Bid (NBB) remains at $5.10, the D-Limit order is now resting outside the NBBO – but the broker doesn’t know this is the case. They may be expecting fills at $5.10 but are very unlikely to receive them.

Our new cancel/reprice functionality gives brokers, on an opt-in basis, the option to have IEX Exchange act upon their D-Limit order in this type of scenario. If a D-Limit order that has been restated following a Signal fire is not resting at the NBBO 10 milliseconds later, IEX Exchange can take one of two actions at the time:

Option 1: Cancel back to the Member

Option 2: Reprice back to the NBBO (if within order’s limit, otherwise to the order’s limit price)

These options are designed to improve hit rates of D-Limit users:

- If a broker chooses to receive a cancel, that cancellation prompts the broker to act upon the order.

- If a broker chooses the “reprice” option, IEX Exchange places the D-Limit order back to the NBBO (likely where the Member assumed their order was already resting), making it more likely to find a contra.

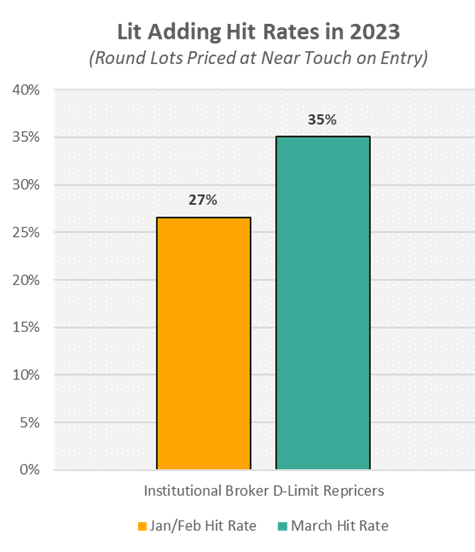

Thus far, the majority of firms opting into this functionality have elected the “reprice” option, and the hit rate increase they have experienced has already been significant.1 The chart below illustrates just that.

The increase from 27% to 35% hit rates is especially meaningful since it does not sacrifice any performance as measured by markouts! D-Limit markouts from Members who have opted into the reprice functionality have remained very similar and, if anything, markouts improved by 1% to 5% of spread across various time horizons.

We are encouraged by these early results and believe they demonstrate that the new functionality successfully solves for IEX Exchange’s objective to deliver best-in-class performance without unnecessarily sacrificing likelihood of fill.

We invite more Members to experiment with this new functionality and hope that they will experience similarly positive results.

1We define hit rate as the % of orders which receive a partial or full fill.

Sam Stevens

Head of Business Analytics