This month we’re introducing a new version of The Signal (a.k.a. Crumbling Quote Indicator), the predictive model that targets adverse price changes and which powers IEX Exchange’s signature protective order types. The Signal is designed* to predict imminent changes to the National Best Bid/Offer (NBBO) and allow order types including D-Peg and P-Peg to react advantageously to unstable market conditions.

Since IEX Exchange’s inception, we’ve updated The Signal five times; the last update was introduced in May 2018. Since then, IEX Exchange released D-Limit, a groundbreaking new order type that incorporates the Signal and which has dramatically changed the market composition of trading on our venue. There have been major changes in overall market conditions since 2018 as well: Retail trading and volatility surged during the Covid-19 pandemic, increasing market volumes as well as the average number of NBBO quote changes. Additionally, three new US equities exchanges have come online, and their presence directly affects the NBBO prediction problem. With all these changes since our last Signal launch, we’re due for an update!

The newest iteration of The Signal – call it V6 – brings a new level of performance for pegged orders on IEX Exchange. Some of its enhancements include:

- Looking at both size and number of venues (rather than just venues)

- Adding 3 new venues (MEMX, MIAX, Nasdaq PSX)

- Shifting from a logistic regression to a rules-based model

Powering Protection Against Adverse Selection

As a refresher, here’s how The Signal works and how it is designed to deliver performance.

When the Signal fires – indicating that it predicts that the National Best Bid or Offer (NBBO) is about to crumble – D-Peg (and P-Peg and C-Peg) orders are restricted from exercising discretion to the midpoint and near-side respectively for up to 2 milliseconds. During this time, they remain at their resting price 1 tick outside the near side of the NBBO and are therefore shielded from execution against all counterparties except very aggressively priced orders (removers priced through the far side of the NBBO). The goal of the mathematical model is to trigger this restriction during moments where the model predicts that the NBBO is about to move against a resting order, resulting in potential adverse selection in the event of a trade.

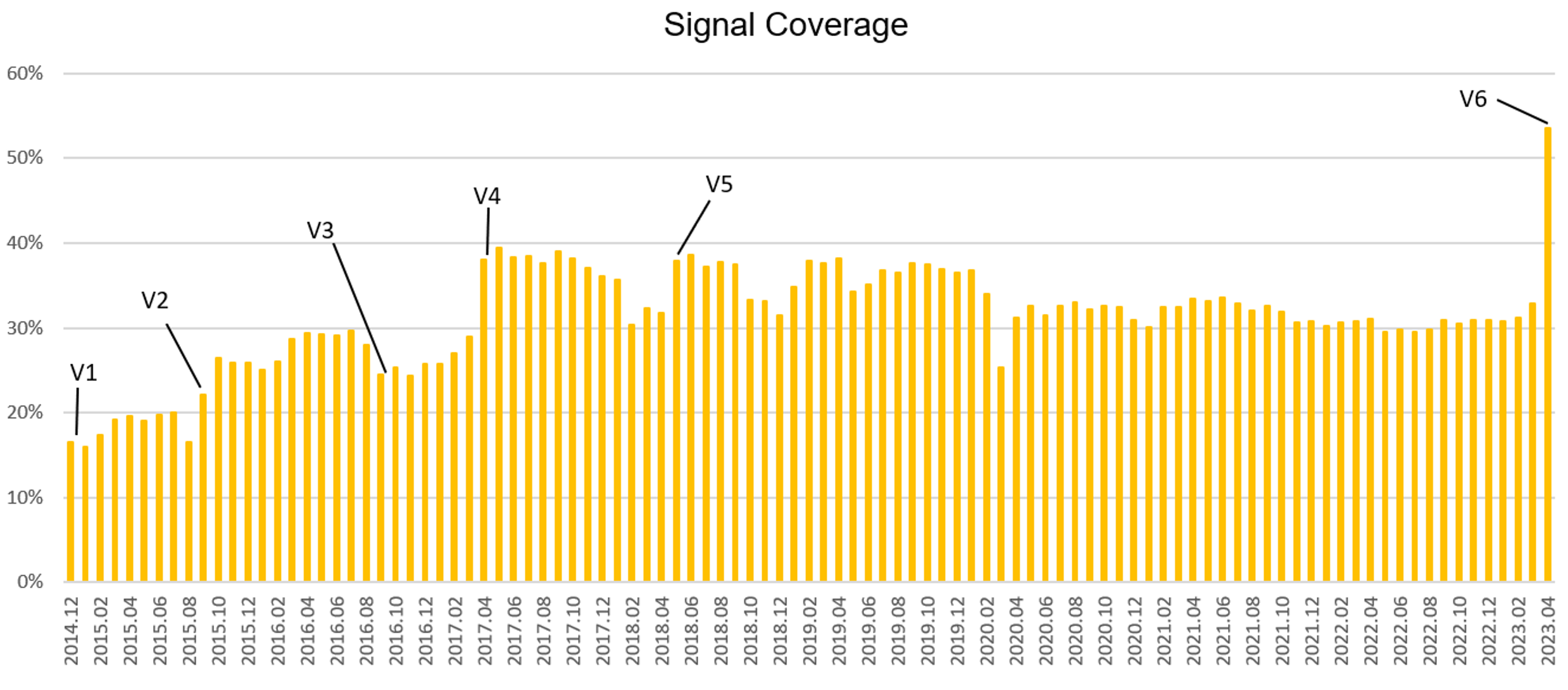

A natural way to think about The Signal’s performance is through two dimensions: coverage and true positive rate. How many NBBO changes does it predict, and how accurate are those predictions when they occur? For coverage, we measure what percent of adverse NBBO midpoint moves occur while The Signal is restricting discretion of our pegged order types. For the true positive rate we can measure what percent of model predictions see the midpoint of the NBBO move below its value at the time of prediction within 2ms.

Of course, we could easily create a trigger-happy Signal with 100% coverage of NBBO changes, but this would come at the expense of its true positive rate (conversely an extremely selective Signal could achieve a very high true-positive rate but might not actually provide much coverage). Our goal with this new version of the Signal was to increase the coverage by 20% at the same target true positive rate as our prior models – and we landed a bit better than that!

The current version of the Signal (V5) predicts 33% of NBBO changes in the volume-weighted average symbol and the new version of the Signal (V6) is predicting 54% of NBBO changes (numbers reported over the week of 4/3/2023-4/7/2023) without sacrificing its true positive rate.

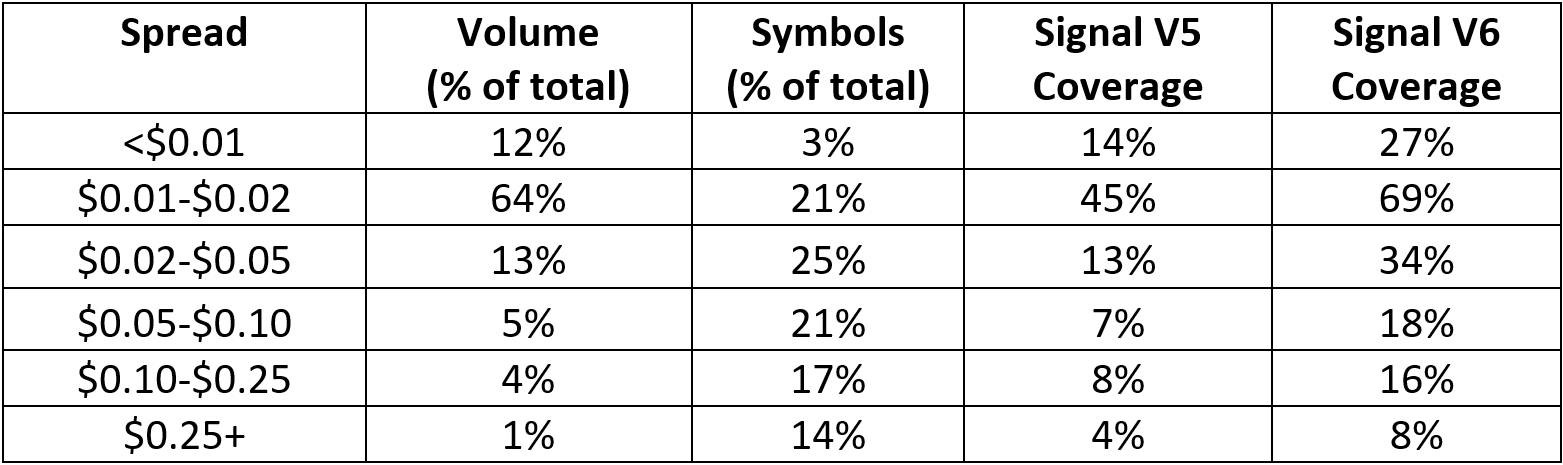

Here’s the breakdown in coverage improvement by spread from the current version of The Signal (V5) to the new version (V6).

Updating The Mathematical Model

So, what’s driving these great results? In V6 of the Signal, the mathematical model is being updated in three main ways:

- Changing from logistic regression to rules-based logic: The logic used to evaluate market data and generate predictions is changing from a standard logistic regression to a rule-evaluation format. Predictions are generated according to a set of explicit rules being satisfied by market data updates. The rules used capture four main categories of events:

a. Disappearing quotes on geographically significant venues

b. Quote-size update bursts

c. Locked or crossed markets

d. Rapid-correlated quote changes

- Online performance evaluation: V6 contains a layer on top of its rules-based logic that monitors each rule’s performance in real-time and allows for adaptive response to changing market conditions over the course of the day. When performance drops outside of expectations, individual rules can be “turned off” and prevented from generating new predictions until their performance returns to normal levels.

- Adding size update data: In V5, the model evaluates and makes a prediction only when the top of book price changes on one of eight venues. In V6, we’re adding three new venues to the set and additionally evaluating the model whenever either the price OR size of any venue’s protected quote changes. This results in the ability for V6 to use quote depth intelligently when making crumbling quote determinations.

Here’s a handy side-by-side comparison:

The result of these changes is a new aggregate statistical model that, like all prior versions of the Signal, is deterministic and reproducible from its market data input. For more detail on the newest model and how it’s being implemented, please see our SEC filing, which includes the formula in full for those interested.

Next Steps & What This Means for Members

In our previous update cycles, we pushed the latest version of The Signal to all Members at once. This time, in response to client feedback, Members are invited to opt in and make the change at their preferred pace. The current production model (V5) will remain the default. Beginning April 18, 2023, clients may elect through a port request form to use the new Signal formula for all of their D-Peg, P-Peg, and C-Peg orders or can designate via a FIX tag to opt-in on a per-order basis (see Trading Alert #2023-008).

Rolling out the new Signal version in this way will allow Members to transition from the current model to the new model for their pegged order types at their own pace (or even elect to stick with their current experience). If desired, this will allow for live A/B testing of comparable models in a way that was not possible in our prior Signal updates.

With market conditions changing rapidly, protection against adverse selection is more important than ever. We’re excited to continue improving the performance of our flagship order types to help democratize access to sophisticated trading tools and continually improve IEX Exchange’s execution quality.

*While IEX Exchange endeavors to utilize data and calculations that it believes to be reliable, IEX Exchange cannot ensure the timeliness, accuracy, reliability or completeness of any data or calculations, including our measure of when we determine the quote to be crumbling.

Luke Kowalczyk

Head of Quantitative Research