In our previous two blog posts about D-Limit, we highlighted the benefits of D-Limit for those who choose to use the order type. Based on our initial data, we showed that D-Limit outperforms displayed orders on other exchanges (demonstrated by better markouts) and, if incorporated optimally, can provide its market-leading performance with no material cost to fill rates.

But D-Limit doesn’t operate in a vacuum. During the approval process for D-Limit, we laid out our expectations for how D-Limit could improve competition and promote public price discovery for the broader market.

In this post, we use five months of D-Limit data (comparing May-September 2020 to October 2020-February 2021) to show how those expectations have come to life in terms of both IEX Exchange’s trading quality and the dynamics of the broader market. We also show how the concerns raised during the approval process have not materialized in the data.

D-Limit in Action

Increasing Displayed Trading

When we filed for D-Limit, we argued that by enhancing performance for displayed orders on IEX, we could incentivize more market participants — and a broader set of firms — to display orders.

Today, a very broad array of firms is using D-Limit on IEX — including full-service broker-dealers, agency broker-dealers, and proprietary trading firms — showcasing the appeal of this innovation to market participants with a range of strategies, perspectives, and levels of technical sophistication.

As a result, displayed trading on IEX has expanded dramatically since the introduction of D-Limit. Displayed volume on IEX Exchange has increased nearly 3x, from 25 million to 73 million shares per day. Of that increase, about 40 million shares per day are from broker-dealers who only display orders on IEX using D-Limit, suggesting that users are seeing consistently high-quality fills from D-Limit and are bringing more displayed orders to the market as a result.

Incentivizing Quotes

To meaningfully improve the quality of displayed trading in the market, however, D-Limit must also drive more public price discovery — meaning more and tighter quotes.

Today, the number of symbols IEX has at the NBBO at any given time has increased 4x (from about 800 before D-Limit to over 3200 after D-Limit). IEX is also at one or both of sides of the NBBO nearly four times more often, from about 10% to 40% of the trading day.

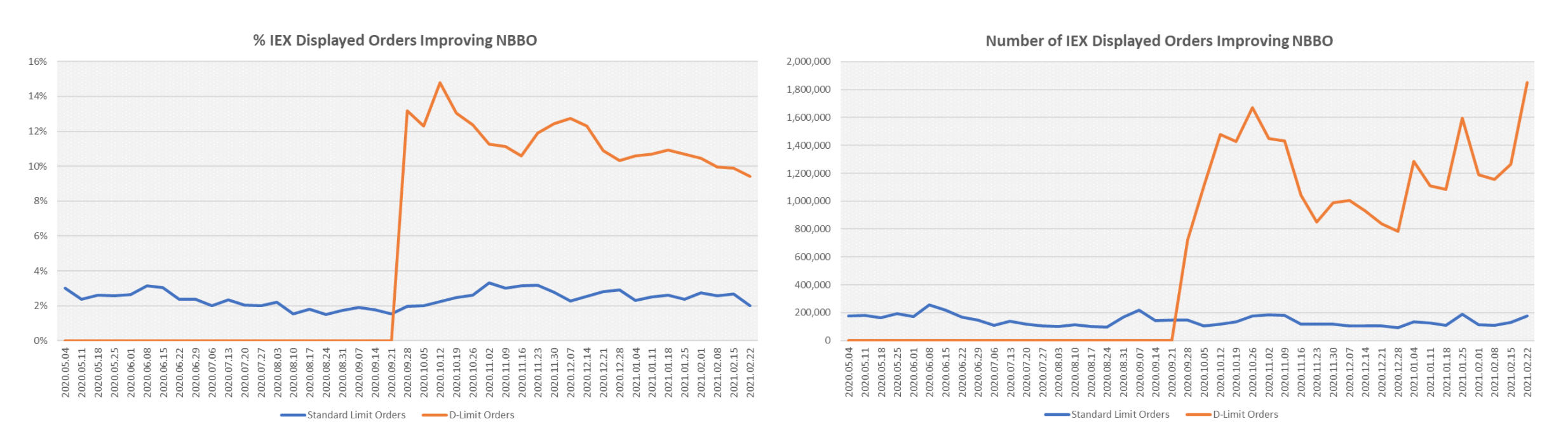

Moreover, D-Limit orders are improving, not just matching, the best prices available. D-Limit orders are setting new best prices in the market (i.e., improving the NBBO) at a rate 5x greater than traditional displayed orders on IEX (about 10% of D-Limit orders are improving the NBBO, compared to just 2% for traditional displayed orders). On top of that, the number of D-Limit orders improving the NBBO is approximately 10x greater than traditional displayed orders.

Displayed volume, increased quoting, and tighter quoting — a new standard for displayed trading has been set.

A Targeted Solution

At the same time that IEX set an ambitious (yet attainable) goal to improve displayed trading in the market with D-Limit, we committed to doing so in a targeted, narrow, and precise manner. That means that the success of D-Limit should not come at the expense of other measures of market quality.

D-Limit’s success on that measure has also been borne out by the data.

Quote Accessibility

First, the introduction of D-Limit has not impaired brokers’ ability to trade against quotes on IEX. Fill rates targeting our quote have remained consistent, showing that the quote remains accessible.

This stems from the fact that, as we’ve demonstrated in the past, only specific, deliberate strategies that capitalize on the information asymmetry that exists during quote changes are likely to attempt to trade around the firing of the Signal with any frequency. We know this because the majority of spread-crossing orders (those that would be trading with D-Limit) that IEX receives from traditional broker-dealers arrive well before our Signal fires — and would therefore not be impacted.

To further demonstrate this and try and determine “impact” from IEX’s perspective, we analyzed the fill rate of orders which we believed to be “targeting” our quote. In other words, we isolated spread-crossing orders whose limits were aggressive enough to interact with an IEX quote (at the NBBO) that existed at least 2ms before the order’s arrival. This view tries to simulate the experience of the “order sender” and allows us to approximate the fill rates they may experience.[1]

This view shows that when controlling for firm type,[2] the fill rates pre/post D-Limit are about the same. It’s also important to note the disparity between the fill rates of institutional broker-dealers and those of proprietary trading firms.

Without knowing the strategies behind such low fill rates for prop orders, one may conclude that their broader strategy does not revolve around receiving high fill rates like those of agency broker-dealers. Another explanation could be that some of these firms were already using strategies that aimed to trade during periods of market transition — when there is inherently more uncertainty about the accessibility of any quote, regardless of order type or venue.

Routing practices

D-Limit also hasn’t meaningfully changed the way that broker-dealers route to IEX or their need to preference our quote. Broker-dealers continue to route to IEX in proportion to how often we are at the NBBO. In fact, when you compare quote targeting orders to the percentage of time IEX is at the NBBO, the dynamics are nearly in lock step.

Narrow focus

Lastly, the Signal continues to be triggered only in very narrow circumstances, which has not changed since the introduction of D-Limit. It is still “on” for a very small number of seconds per symbol per day.

A New Standard for Displayed Trading

Ultimately, the data demonstrates that D-Limit isn’t just providing a benefit to the market participants who choose to use it. D-Limit is raising the bar for displayed trading overall, showing that targeted innovation can make a difference to the quality and sustainability of our equity markets.

As always, please reach out to me or your IEX contact if you have any questions or would like to collaborate on more in-depth analysis of your data.

[1] We also perform some logical adjustments to the actual fill rate calculation. For example, if a 300-share order is targeting a 1,000 share quote, the fill rate calculation is 300/300. Additionally, if a 300-share order targets a 200-share quote and happens to trade all 300 shares, the calculation is 200/200 — fill rate cannot exceed 100%.

[2] IEX classifications are on a best efforts basis by Member firms’ trading sessions.

Co- Founder and Chief Operating Officer, IEX Group