The stock market exists to serve investors. American households own $38 trillion worth of equities — more than 59 percent of the U.S. equity market — either directly or indirectly through mutual funds, retirement accounts and other investments. To best represent the voices of U.S. investors, we went directly to the investor community to hear their perspective on how Regulation NMS could be modernized to better support their needs.

In December 2022, the SEC shared four distinct proposals to update U.S. equity market structure:

1. Regulation NMS: Minimum Pricing Increments, Access Fees, and Transparency of Better Priced Orders

2. Disclosure of Order Execution Information

Of these four proposals, the Regulation NMS proposal most directly represents an opportunity to update the rules of the current national market system to make the stock market more transparent and competitive for investors. Reg NMS, as it’s known, was last updated in 2005 – nearly twenty years ago.

To better understand investors’ perspectives on the nuances of ideas covered in the Reg NMS proposal, we surveyed the buyside in spring 2023 and heard back from 217 institutional investors across mutual funds, pensions, endowments, hedge funds, RIAs, and private wealth funds. Here’s what they told us:

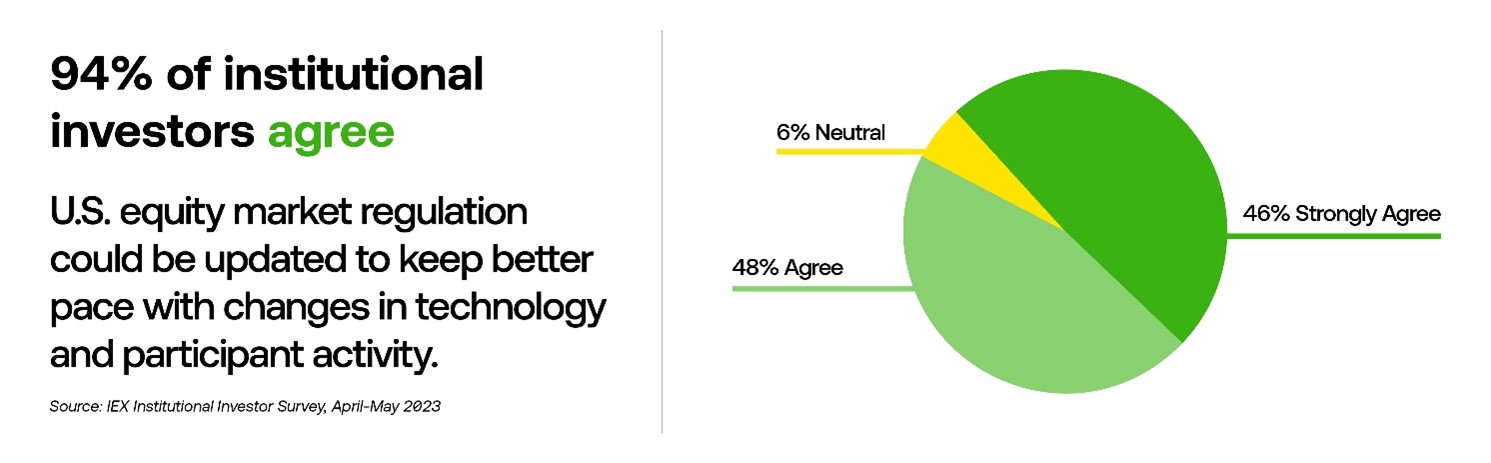

94% of institutional investors surveyed agree that U.S. equity market regulation could be updated to keep better pace with changes in technology and participant activity.

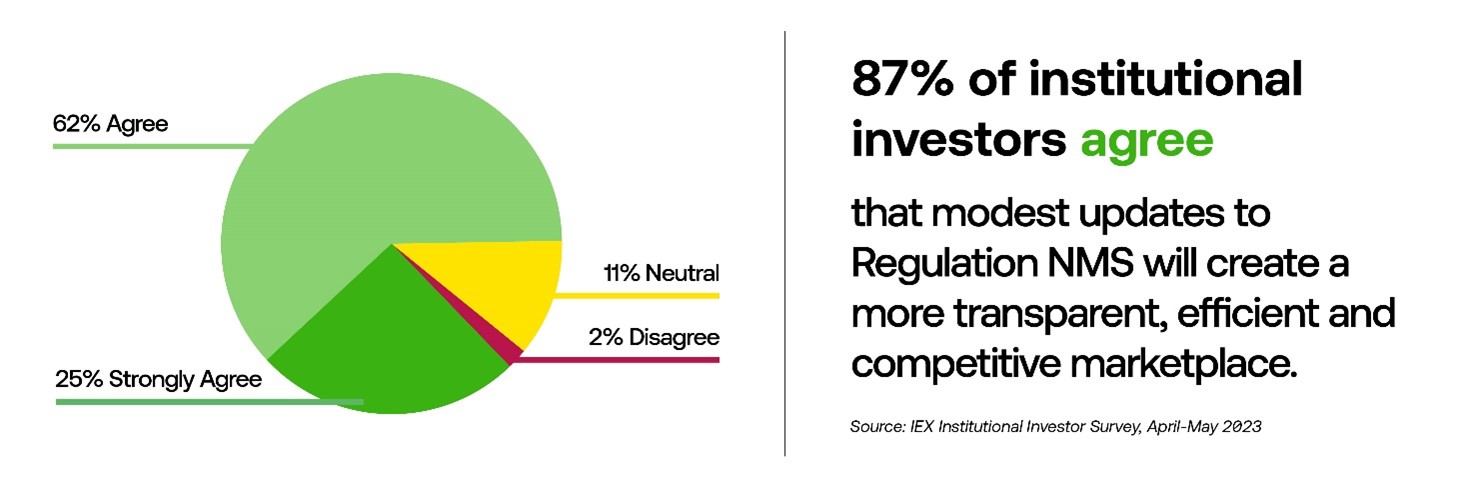

87% of institutional investors agree that modest updates to Regulation NMS will create a more transparent, efficient, and competitive marketplace.

Tick Sizes

Today all symbols are quoted in penny-wide increments. As part of this new Reg NMS proposal, the SEC has proposed narrowing this quoting increment for symbols they define as "tick/quote constrained."

For instance, the SEC's estimates indicate that ~1,700 symbols, which account for 64% of market volume, would have tick sizes of 10 or 20 mils.

The SEC has proposed 3 new quoting increments in addition to the current penny wide increment:

· 10th of a penny (10 mils)

· 5th of a penny (20 mils)

· 1/2 penny (50 mils)

· 1 penny (existing)

Learn more about the SEC’s proposed ideas relating to tick sizes.

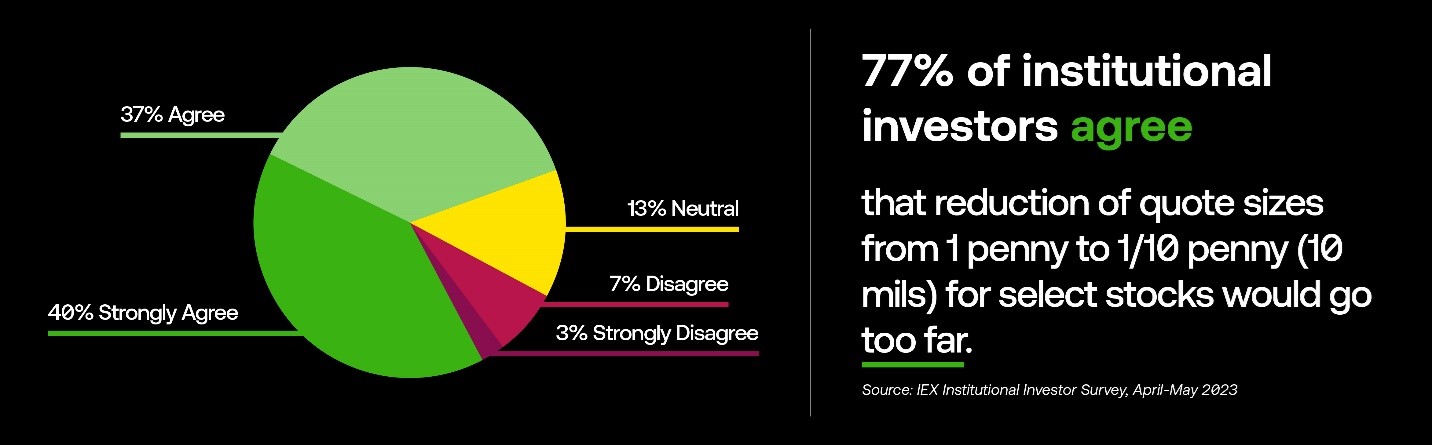

77% of institutional investors surveyed agree that the reduction of quote sizes from 1penny to 1/10 penny (10 mils) for select stocks would go too far.

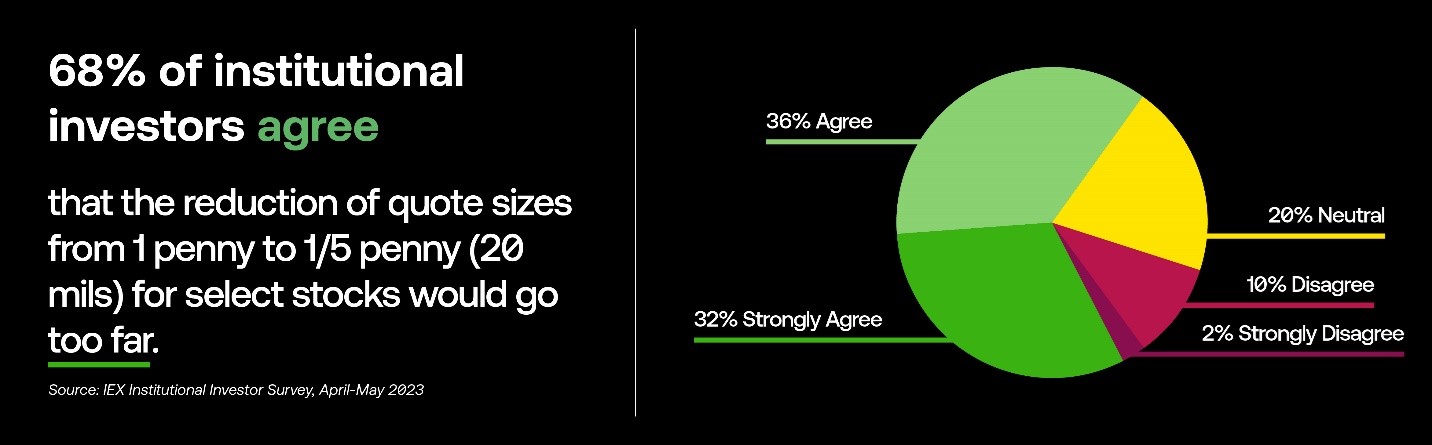

68% of institutional investors agree that the reduction of quote sizes from 1 penny to 1/5 penny (20 mils) for select stocks would go too far.

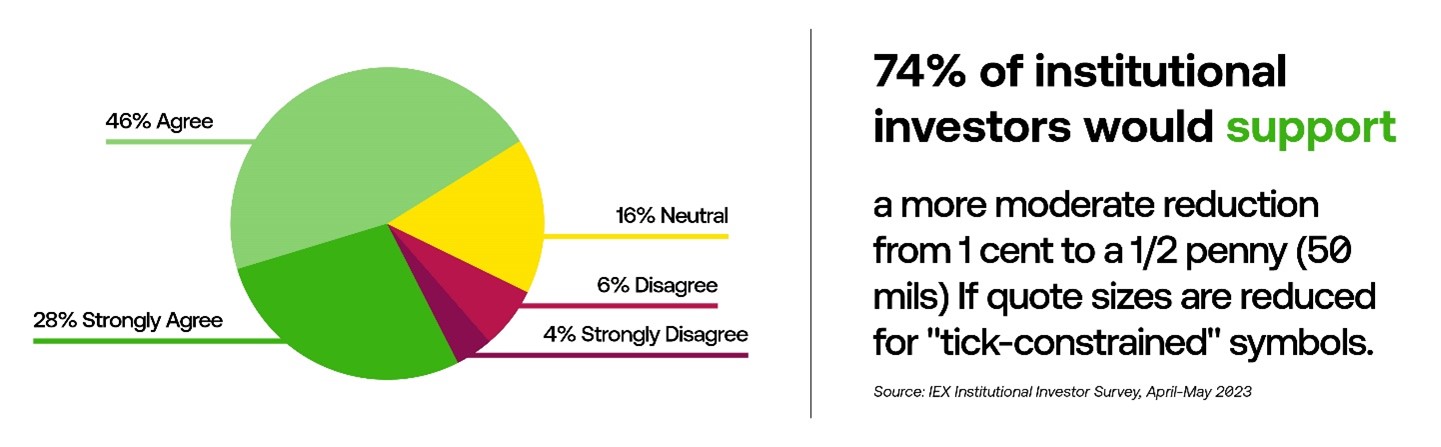

74% of institutional investors would support a more moderate reduction from 1 cent to a 1/2 penny if quote sizes are reduced for "tick-constrained" symbols.

As an additional data point: of the asset managers and pensions that actively submitted public comment letters to the SEC on the market structure proposals, 100% wrote in favor of a tick size reduction to 50 mils for “tick-constrained” symbols.

Access Fees

The access fee cap refers to the most a stock exchange is allowed to charge takers of displayed liquidity. That fee, which was adopted in 2005, is still capped at 30 mils/share. At the time, this cap was set at the “going rate” that exchanges were already charging; the rule was meant to guard against exchanges charging excessive access fees as a "toll" to be able to trade with protected quotes. Today, the majority of exchange trading volume (over 85%) trades on exchanges that charge the maximum 30-mil fee – but technological efficiencies have changed the economics and exchanges now pay most of it back as a rebate to incentivize order flow.

Contained within the Reg NMS proposal is a recommendation from the SEC to reduce this access fee cap to a new maximum of 10 mils. The SEC proposal aimed to update access fees to match the overall reduction in the cost of technology and lower commission rates to brokers (which means exchange fees are now a larger percentage of costs), and to reduce exchange price complexity driven by high access fees.

Learn more about the SEC’s proposals relating to exchange fees.

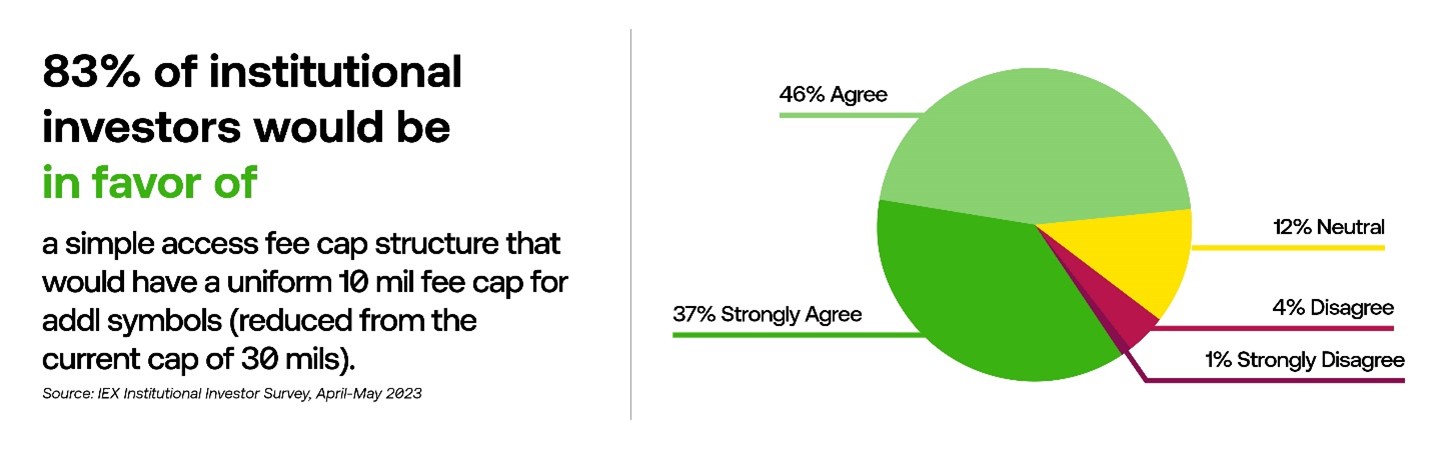

83% of institutional investors would be in favor of a simple access fee cap structure that would have a uniform 10 mil fee cap for all symbols (reduced from the current cap of 30 mils).

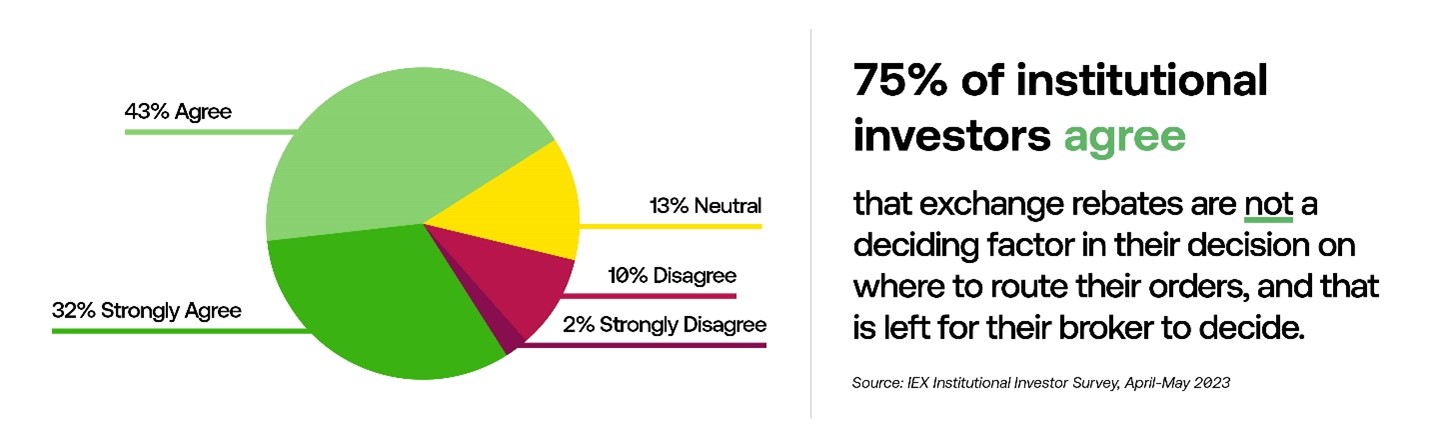

75% of institutional investors agree that exchange rebates are not a deciding factor in their decision on where to route their orders, and that routing is left for their broker to decide.

Rebate Tiers

Most exchanges today have created volume-based pricing tiers also known as “rebate tiers.” A 2021 analysis from RBC found “at least 4,025 separate factors that can ultimately determine the fees charged and rebates offered by exchanges" which “strongly suggests that exchange prices are tailored and offered on a bespoke basis” and “adds additional complexity to the ecosystem.” The goal of these tiers is to incentivize more liquidity posting: the reward is a higher rebate based on posting levels achieved. There is a lot of frustration from the broker community regarding the lack of transparency around these tiers and the inability of all but a few to be able to reach any level of a rebate tier.

At IEX Exchange, we believe that rebate tiers represent a conflict of interest and that exchange fees should be clear, simple, and transparent. See our fee schedule here.

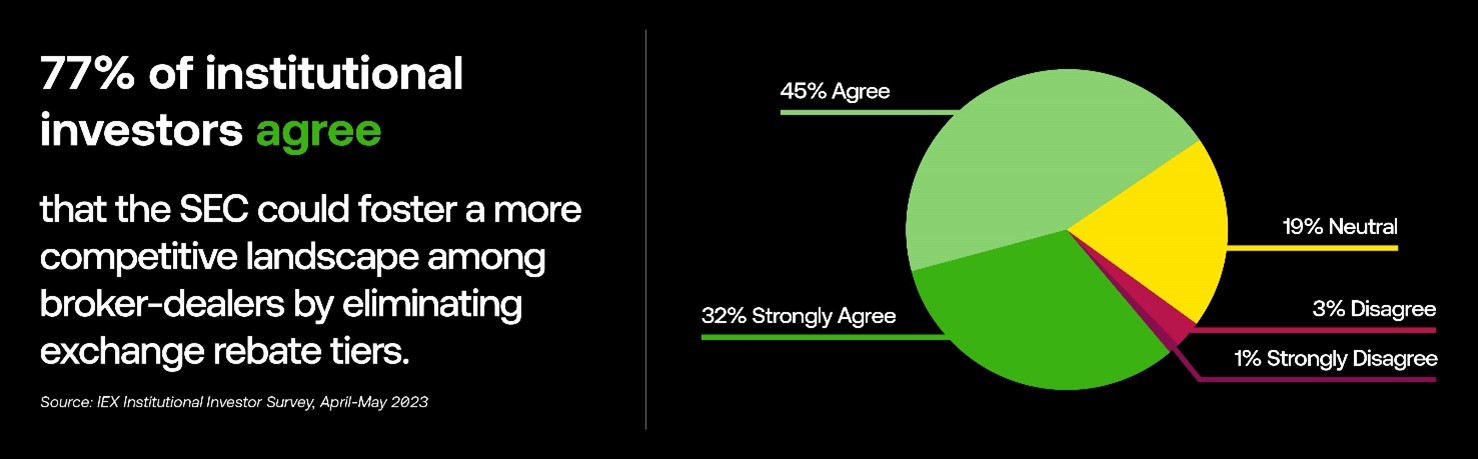

77% of institutional investors agree that the SEC could foster a more competitive landscape among broker-dealers by eliminating exchange rebate tiers.

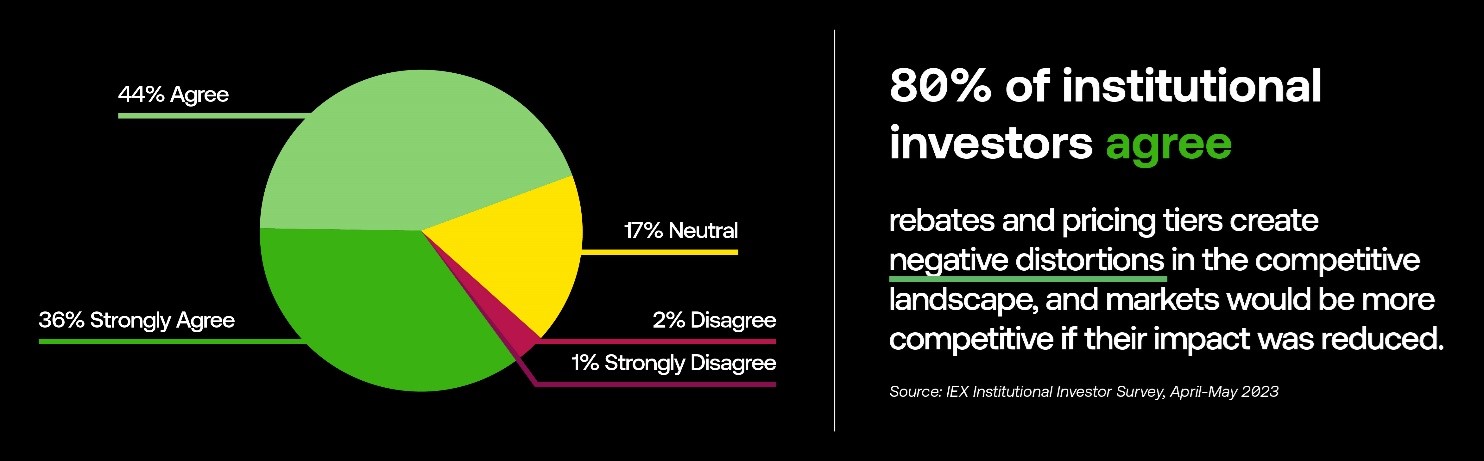

80% of institutional investors agree that rebates and pricing tiers create negative distortions in the competitive landscape, and markets would be more competitive if their impact was reduced.

Odd Lots

Historically, stock markets have displayed their prices in “round lots.” In almost all cases, a round lot is equal to 100 shares. As of last April, only 11 listed stocks, with high per share stock prices, had a round lot size other than 100. Nine of these had a round lot of 10 shares, and two (including Berkshire Hathaway, the undisputed champion of high-priced stocks) had a round lot of a single share.

The distinction between round and odd-lots matters for various reasons.

1. Only round lots count toward determining the national best bid and offer (NBBO), which is the basic equities benchmark all participants rely on to define the best quoted price and to measure the degree of “price improvement” an investor receives on a given trade.

2. Only the best round lot bids and offers on each exchange are protected from being “traded-through” –meaning firms can’t execute a trade at a worse price without seeking to access the exchange quote.

3. The consolidated tape feeds published by the exclusive securities information processors (SIPs) don’t carry odd-lot quotes, so those quotes are visible only to people who pay for more expensive exchange proprietary data feeds. In contrast to quotes, odd-lot trades have been carried on the consolidated tape since 2013.

Learn more about the SEC’s proposed changes relating to lot sizes.

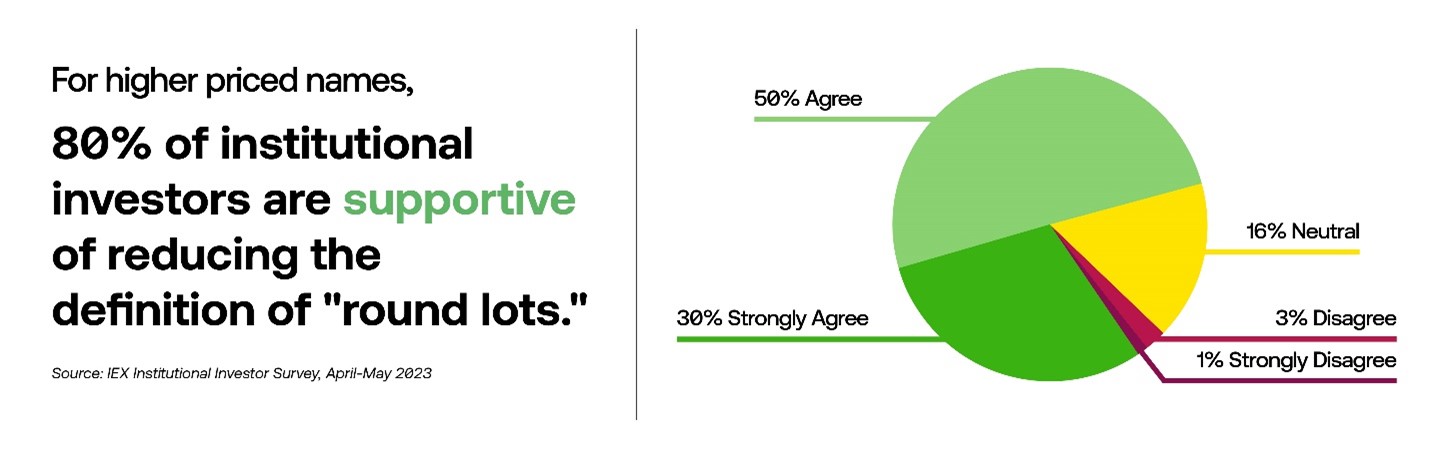

80% of institutional investors are supportive of reducing the definition of “round lots” for higher priced names.

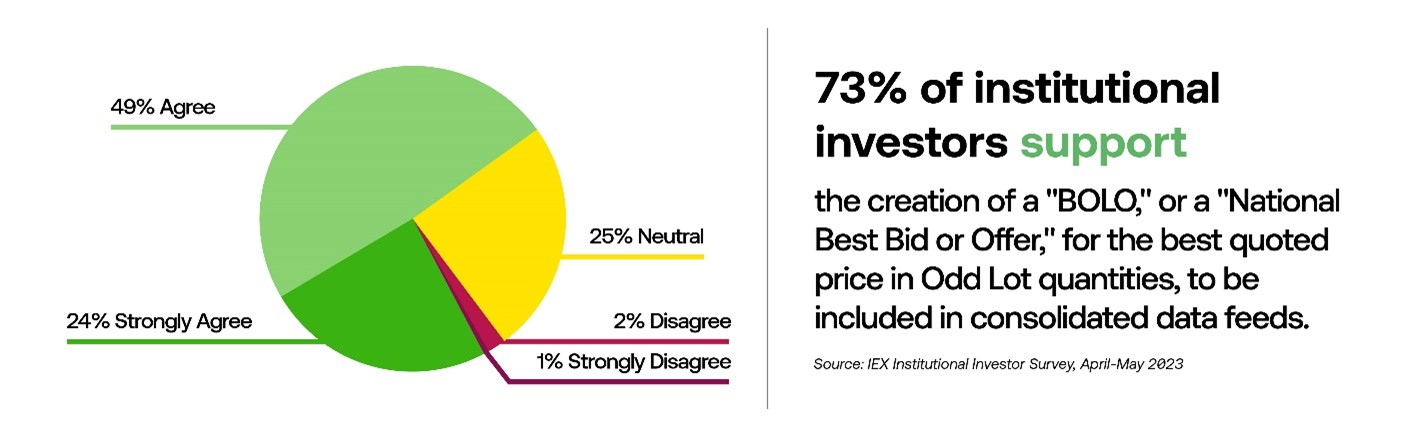

73% of institutional investors support the creation of a "BOLO," or a "National Best Bid or Offer" for the best quoted price in Odd Lot quantities, to be included in consolidated data feeds.

Methodology

The IEX Institutional Investor Survey surveyed 217 market participants in April and May 2023. The survey respondents consist of institutional investors including Pensions, Hedge Funds, Mutual Funds, and Endowments – among others. The AUM of the firms represented ranged from less than $1 billion to over $1 trillion with the majority of respondents from firms that had between $1B and $500B in AUM. Respondents were asked to rank their views on the recent Reg NMS proposals on a Likert Scale.

This blog post and its contents (collectively, the “post”) are provided for informational purposes only and should not be construed as professional advice. The post is based on results of a survey conducted by Investors’ Exchange LLC (“IEX Exchange”) between April 2023 and May 2023 in connection with the Securities and Exchange Commission’s recent proposed amendments to Regulation NMS (the “Survey”). IEX Exchange has no obligation (express or implied) to update or correct any or all of the post or to advise any reader or recipient of the post of any changes or corrections. While every effort has been made to ensure the accuracy of the post, there is no guarantee that the post is complete or correct. The post should not be assumed to be conclusive in whole or in part. IEX Exchange makes no representation or warranty, express or implied, as to the accuracy, completeness or reliability of the post. Any reliance on the post is at the reader’s own risk. IEX Exchange assumes no liability or responsibility for the post or any errors, omissions, opinions or mischaracterizations contained herein or for any actions taken (or not taken) in reliance on all or any portion of the post.

If you have any questions or comments regarding the post or the Survey, please contact bdteam@iextrading.com.

Ronan Ryan

Co- Founder and Chief Operating Officer, IEX Group