This is the second and last part of a two-part series of market structure blog posts. The first part is here. Feedback and suggestions more than welcome at benjamin.connault@iextrading.com.

In the first part of this series, I discussed the triggering of a Market Wide Circuit Breaker (“MWCB”) halt and price discovery on primary exchanges during the halt. In this second and last part, I describe price discovery on secondary venues and across venues, discuss the end of a MWCB halt, and conclude.In the first part of this series, I discussed the triggering of a Market Wide Circuit Breaker (“MWCB”) halt and price discovery on primary exchanges during the halt. In this second and last part, I describe price discovery on secondary venues and across venues, discuss the end of a MWCB halt, and conclude.

3) Price discovery during a MWCB Halt: on secondary venues and across venues

Price discovery mainly happens on the primary exchange during a MWCB halt (see previous section). However, many secondary trading venues allow some limited price discovery, for example via the maintaining or canceling of displayed limit orders.

How much price discovery happens on secondary trading venues? How does price discovery work across exchanges in this fragmented environment? Are traders maintaining prices in line between venues, using the limited means at their disposal? Are MWCB trading rules on secondary exchanges helping or harming overall price discovery? We look at these questions in this section.

No secondary exchange accepts new orders during a MWCB halt. Furthermore, there are again some differences between MWCB exchange rules. The Cboe exchanges make their continuous books dark during the halt. New orders and order cancels can be queued to be effective upon resumption of trading, but no order book updates are sent during the halt. Other exchanges, including Nasdaq, ARCA and IEX, keep their order books alive, accepting order cancels and disseminating real-time updates through their proprietary feeds.

Here is a count of order cancels received during the 3/9 halt by Nasdaq (XNGS) and ARCA (ARCX) in non-listed symbols (log scale):

Other exchanges, including Nasdaq, ARCA and IEX, keep their order books alive, accepting order cancels and disseminating real-time updates through their proprietary feeds.

The chart demonstrates that traders take advantage of the limited price discovery mechanisms available to them on secondary trading venues. Traders were clearly canceling orders throughout the MWCB halt, with a notable peak in canceling activity between 09:40:30 and 09:43:00.

At this point, we know that price discovery for a given stock is happening on more than one venue, i.e., in a fragmented way. But how does this price discovery work across venues?

Let’s first look at some data for SPY. SPY is listed on ARCA. The below chart is a representation of the Nasdaq order book for SPY, as seen through second-level snapshots between 09:20 and 10:00. The chart tracks how deep in the book you need to go to find a given number of shares. The grey area between the buy side and the sell side is the spread of the Nasdaq order book — typically 1 cent wide during continuous trading, and 50 cents to $1 wide during the MWCB halt. The yellow line is the ARCA auction indicative match price leading to the MWCB reopening auction.

In SPY, like in other names, entering a MWCB halt causes many market participants to cancel some of their resting orders. This leads to an immediate spread widening. On 3/9, SPY last traded at $276.35 before the MWCB halt, and reopened at $276.30. Throughout the MWCB halt, the ARCA auction indicative match price remained within the Nasdaq order book spread. Price discovery was orderly.

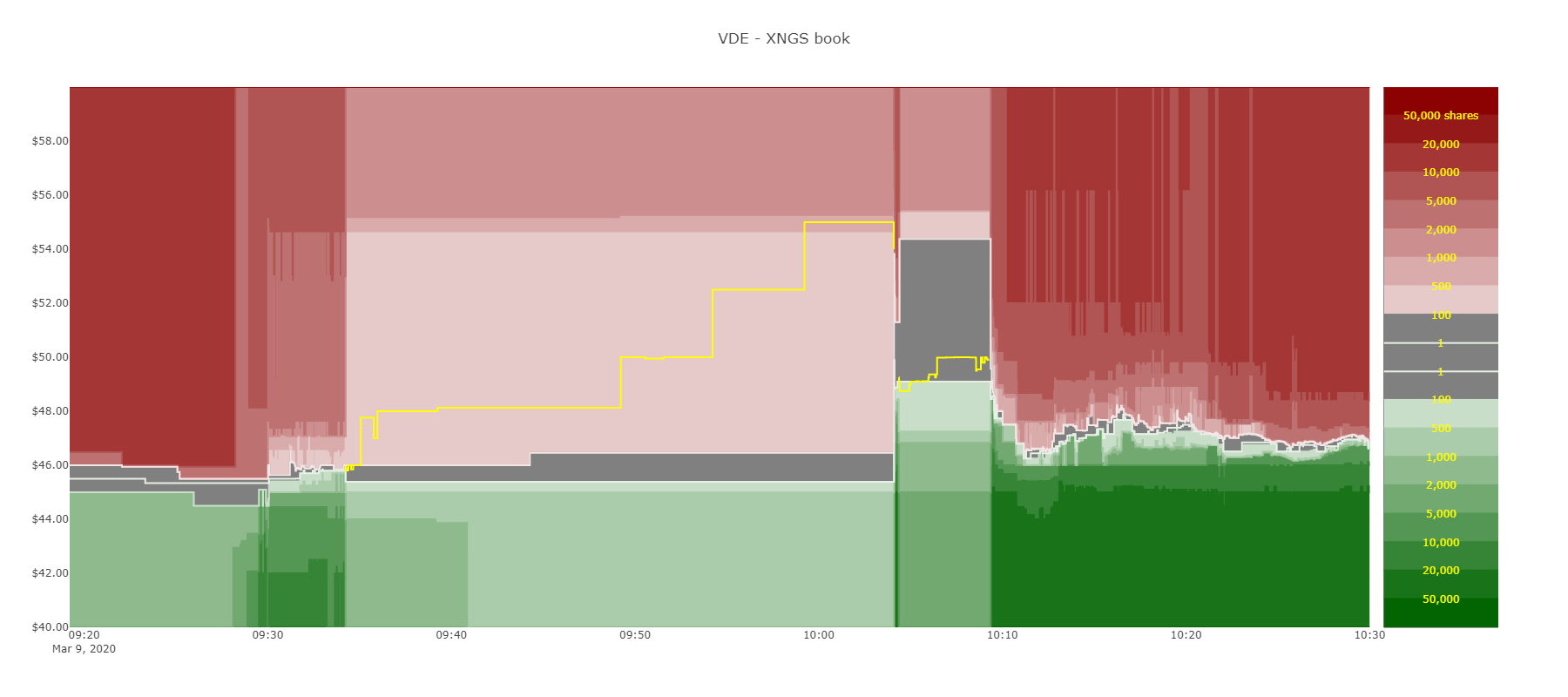

Let’s now look at VDE, the Vanguard Energy ETF, also listed on ARCA. As opposed to SPY, VDE moved significantly during the MWCB halt. VDE traded last at $45.84 before the halt and reopened at $54.00. VDE did not reopen at 09:49:13 (the end of the 15-minute MWCB halt). Rather, the re-opening auction was extended three times. This is because ARCA applies auction collars to its reopening auctions and extends the auction for 5 minutes with updated collars, until the auction is able to cross within the collars. VDE reopened at 10:04:05. Interestingly, it only traded for 16 seconds before entering a LULD halt.

As opposed to what happened for SPY, the ARCA auction indicative match price for VDE quickly moved outside of the Nasdaq auction book spread after the MWCB halt started:

The VDE example provides an opportunity to study price discovery across venues during a MWCB halt. Because Nasdaq only accepts order cancels, price discovery on Nasdaq can only happen through the cancellation of Nasdaq orders on the ask side as the ARCA auction indicative match price moves up. (Note: because the book is very thin to start with, we are looking at orders from only a handful of traders and should be mindful of generalizations.)

Here is the state of the Nasdaq order book as of 09:35, 09:45 and 09:50 (when the ARCA auction prices were $46.00, $48.13 and $50.00 respectively). Between 09:50 and 10:04:05 (around the reopen), there were no additional order cancels other than two inconsequential orders prices at $0.01 and $199,999.99. The auction price went up briefly to $55.00. VDE opened at $54.00.

The takeaways from the order book activity are mixed. There is some amount of order cancellation, but some sell orders remain on the book deeply below current prices as reflected by the ARCA auction messages (e.g., 1 order at $46.46 and 1 order at $48.35). However, these orders are successfully canceled around the reopen (see next section), so it is possible that the traders left their orders on the book with the confidence that they would be able to cancel them at the last moment. Since Nasdaq does not accept new orders during the MWCB halt, there is some option value in keeping an order on the book, even at a dislocated price. Finally, most exchanges will cancel an order upon resuming trading if it crosses the reopen quote, limiting the risk of leaving orders on the book at dislocated prices.

Overall, price discovery on secondary exchanges is very limited by the exchange rules in place during a MWCB halt. A preliminary conclusion may be that there is very little scope for secondary exchanges to either contribute or harm price discovery. If that is true, leaving the books open during a MWCB halt (like Nasdaq or IEX) or essentially shutting them down (like the Cboe exchanges) are both reasonable options. However, it is notable that VDE was halted again after 16 seconds of trading. Further scrutiny may be needed to assess whether price dislocations across venues contributed to this second halt.

4) Exiting a MWCB Halt

While the SIP is responsible for triggering a MWCB halt, the primary exchange is the one responsible for exiting the halt. Other exchanges wait for the primary to reopen trading. The primary attempts to reopen the stock via an auction. The auction typically takes place exactly 15 minutes after the start of the MWCB halt, but it can sometimes be later, as in the VDE example of the previous section. If there is not enough interest for an auction cross, trading can also resume without an auction. Some of the details are exchange specific. As an example, BZX-listed symbol BBEU reopened at 09:49:13 without an auction print, traded first on ARCA at 09:50:10, and did not trade on BZX before 09:51:43.

In theory, fast traders can observe the reopening on the primary market and react on other venues before the other venues themselves observe the reopening. This is a standard feature of a continuously-trading fragmented market. The end of a MWCB halt is no exception.

In practice, are fast traders leveraging this ability? Yes, at least sometimes. Keeping VDE as an example, the table below shows that 3 sell orders were canceled after ARCA reopened, but before Nasdaq did.[1] Furthermore, those orders include precisely the two orders that are priced more aggressively than the reopening auction price on ARCA.

The fact that U.S. market structure leaves room for this type of latency-sensitive behavior is not necessarily a problem, although it sometimes can be. At minimum, the EBAY (see Table 2) and VDE (see Table 4) examples are good reminders that entering and exiting MWCB halts are fragmented events which require coordination across venues and leave room for latency races — like pretty much everything else.

5) Conclusion

The four March 2020 MWCB episodes were significant market structure events. In this blog post, I gathered some initial data around those events. More work is needed to understand the full impact of the MWCB halts on the volatile markets of March 2020. I do not aim to reach definitive conclusions about potential flaws or fixes here. However, some take-aways already emerge:

- The MWCB functioned well.

- SPX lags price discovery before and around the open.

- There are nontrivial differences in MWCB rules across exchanges.

- There is a limited amounted of price discovery on secondary trading venues. More work is needed to understand if it is helpful, harmful or neutral.

- Entering and exiting MWCB halts are fragmented events that leave room for latency races.

- Only proprietary exchange market data feeds provide real-time information during a MWCB halt.

Some topics that deserve further scrutiny include the coordination between cash and futures, a more systematic study of the contribution of secondary venues to price discovery, LULD halts around a MWCB halt, the interaction of short-sale restrictions with MWCB halts and reopening auctions, and the role of auction collars.

[1] In fact, 1 order appears to have been canceled 1.7ms before ARCA reopened. This is likely to be a timestamp illusion.

About IEX

Launched in 2016, the Investors Exchange is a stock exchange working to protect investors. In just three years, the Investors Exchange has grown to be one of the Top 10 largest exchange operators, globally, by notional value traded. To learn more about the exchange and other IEX businesses visit www.iextrading.com or search IEX.

©2020 IEX Group, Inc. and its subsidiaries. Neither the information, nor any opinion expressed herein constitutes a solicitation or offer to buy or sell any securities or provide any investment advice or service. The information herein is believed to be reliable, but the Firm makes no representation as to the accuracy or completeness of, and undertakes no duty to update, information herein and any and all liability is expressly disclaimed relating to or resulting from use of this information.

This document may include only a partial description of the IEX product or functionality set forth herein. For a detailed explanation of such product or functionality, please refer to the IEX Rule Book posted on the IEX website:www.iextrading.com.