.webp)

In March 2020, the S&P 500 fell more than 30% in less than a month. While the market recovered and set new highs just five months later, it’s clear by now that the shock of that era has had a lasting impact on the market in other ways.

Three years later, we wanted to unpack some of these shifts, the effects they’ve had on the U.S. stock market, and what it means for investors as we all settle into a “new normal.”

More Volatility = More Volume

No change to the stock market was more fundamental than the rise in volatility.

Looking at the daily average number of NBBO changes per symbol, we see that volatility spiked by roughly 4x in March 2020 vs. March 2019 levels. While volatility subsided somewhat in late 2020 through 2021 before surging again in 2022, volatility seems to have found a new normal with peaks more than twice as high as 2019 -- and where the new lows are higher than the old highs.

IEX Exchange’s D-Peg and D-Limit order types are specifically designed to help investors avoid adverse selection at times right before the NBBO changes, thanks to the unique protection enabled by the Speed Bump and the Signal. In today’s “new normal”, these order types become even more valuable.

As volatility has persisted, so too have elevated levels of stock market trading volumes. In 2019, monthly trading volumes market wide averaged less than 8 billion shares a day. March 2020 saw that number skyrocket, setting a record month for market volumes at over 15.5 billion shares per day. While that number has come down, it has settled into a new normal range, averaging nearly 12 billion shares per day in 2022, a 70% increase vs. 2019. While this elevated level of volume seems great for price discovery on the surface, much of this new volume is occurring outside of traditional on-exchange, single-stock trading, so liquidity in certain names may not be as ample as it seems.

The Rise of the Retail Trader

It’s not just that volumes are up, but the type of trading volume has shifted too.

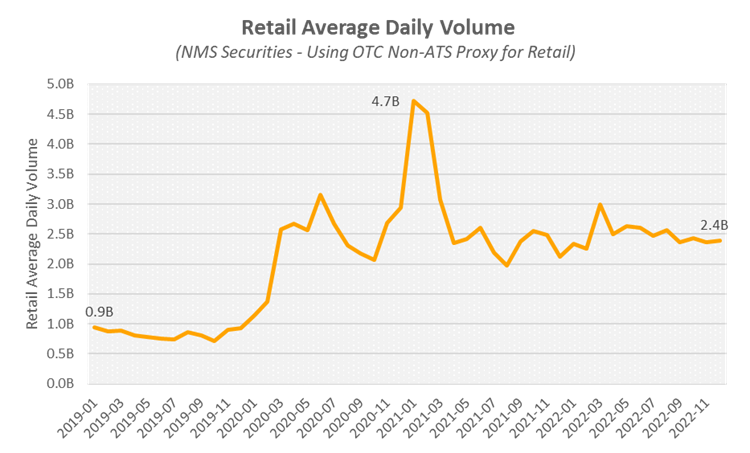

The pandemic coincided with the advent of zero fee and fractional trading becoming mainstream across retail brokers. Retail trading rose steadily over the course of lockdowns to a peak in January 2021, when "meme stock" virality brought retail trading to average nearly 5 billion shares per day (using FINRA OTC Non-ATS as a proxy for retail volume). This was up more than five times from November 2019!

While the number has subsided somewhat, the average level of retail activity has maintained a "new normal" range between two and three billion since 2021, roughly three times higher than before the pandemic.

Much of that retail trading is also occurring off-exchange. While the percentage of total volume executed off-exchange peaked in January 2021 at 47.2%, it has still remained elevated: 2023 Q1 is on pace to be the highest quarter of off-exchange market share ever at more than 45%.

The rise of retail has also brought about a rise in trading for sub dollar stocks (i.e. stocks priced below $1, which have separate rules for quoting and trading on exchanges). Sub dollar volume as a percentage of the market hit record highs above 13% in January 2021, but that record was since surpassed in January 2023 at 13.7% of market volume.

Volume Shifting Away from Inverted Venues

Exchanges with inverted pricing structures have also experienced lasting change from the pandemic. Many of today’s legacy exchanges like NYSE and Nasdaq have “maker-taker” pricing models where the trader “making” the market (by placing a buy or sell order) is incentivized with a rebate payment, while the trader “taking” the other side of that trade pays the transaction fee. An inverted venue like EDGA flips that structure to “taker-maker” – where the “maker” pays the fee, and the “taker” is paid a rebate.

The four inverted venues (EDGA, BYX, BX, and NYSE National) comprised nearly 10% of single-stock market volume in 2019. Inverted venues' differentiated pricing is often used by market participants to “jump the intermarket queue” since these are the venues takers of liquidity are likely to access first. The ability to do this is especially valuable in tighter-spread stocks. So as volatility in March 2020 caused spreads to widen drastically, inverted venues lost substantial market share.

Yet even as the pandemic went on and spreads slowly contracted to within shouting distance of where they were before, inverted venues failed to recapture any of that lost market share and continued to decline to new lows of less than 3% of single-stock volume in early 2023.

At IEX Exchange, we have seen increased volume at the end of the day: a time when inverted venues used to have substantially higher levels of trading. Because IEX Exchange does not pay rebates to either party, our fee structure sits somewhere in-between that of a “maker-taker” and “taker-maker” venue.

A Lopsided Smile for Intraday Volume

The pandemic has also had an enduring effect on the intraday volume curve. In general, U.S. stock market volumes tend to follow a tilted "smile" shape: with elevated volumes at the market’s 9:30am ET open and the beginning of the day, trailing off in the middle of the day, before coming back even higher than before and peaking right at the end of the day with the closing auction at 4:00pm ET. While that smile shape still holds true, the pandemic shock lessened the severity of its arc, bringing more volume to the morning just after market open, with relatively less at the end of the day.

We see this as a second-order effect of persistent volatility and the rise of retail trading, as traders seek to participate in the morning price discovery process and react to pricing opportunities as the market gyrates. We see evidence of this theory in the fact that increases in the percentage of volume traded in the morning have been correlated with increases in volatility over the past few years.

The market is ever-changing and will keep shifting. But for now, three years after COVID-19 shut down the world and caused a seismic shift in the markets, we are still feeling its aftershocks in where, and how stocks trade in this “new normal.”

Sam Stevens

Head of Business Analytics